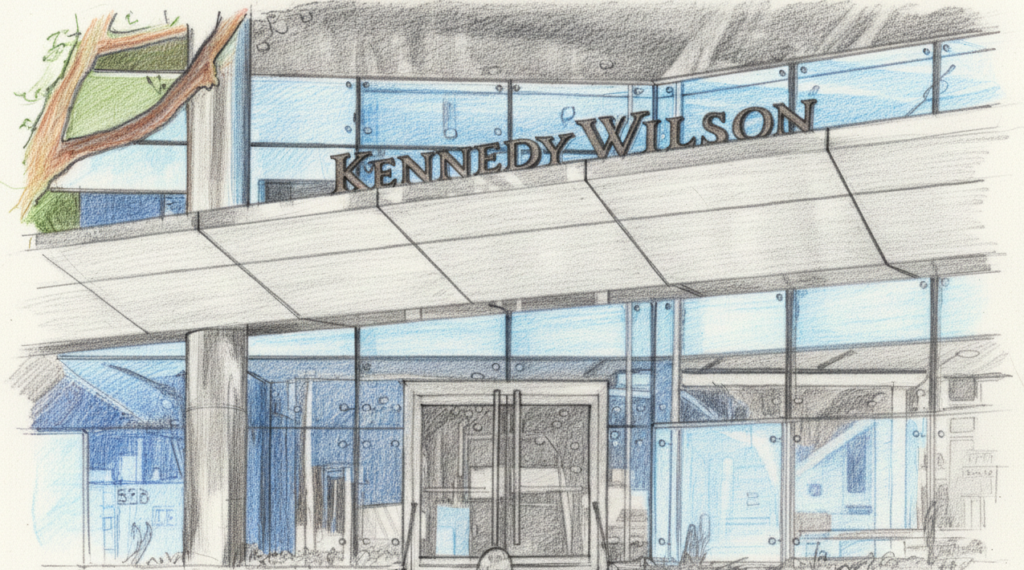

Delaware Shareholder Launches Legal Assault to Block $1.65 Billion Kennedy-Wilson Take-Private Deal

America ı By Rachel Moore

181 0 Comments

A major stockholder has filed a class-action lawsuit in Delaware Chancery Court seeking to halt Kennedy-Wilson Holdings’ $1.65 billion take-private transaction, arguing the deal violates Delaware’s landmark anti-takeover statute and cannot legally close without a supermajority vote of disinterested investors.

In the complaint filed Thursday, plaintiff Bruce Taylor contends that the buyer consortium — led by Kennedy-Wilson chair and CEO William McMorrow and Canadian insurance giant Fairfax Financial Holdings Ltd. — became “interested stockholders” under Section 203 of the Delaware General Corporation Law months before the merger agreement was signed, triggering heightened voting requirements that the current deal structure ignores.

Section 203 is designed to protect public companies from coercive takeovers. It prohibits a merger with an “interested stockholder” (anyone owning 15% or more of voting power) for three years unless the board pre-approved the transaction that created the interested status or the deal receives approval from two-thirds of the disinterested shares.

Taylor alleges that Fairfax already beneficially owned more than 15% of Kennedy-Wilson’s voting power (approximately 28% when including warrants) well before the deal was announced. The lawsuit points to a November 4, 2025 joint bidding agreement between Fairfax and a McMorrow-controlled entity in which the parties agreed to “work together in good faith” to pursue the transaction — an arrangement that, under the broad definition in Section 203, imputes ownership and makes the entire consortium “interested stockholders.”

Because the Kennedy-Wilson board never publicly disclosed pre-approval of the consortium’s formation, the plaintiff argues the merger can only proceed with the two-thirds supermajority vote of unaffiliated stockholders — not the simple majority currently required under the merger agreement.

The $10.90-per-share all-cash offer, announced this week, represents a 46% premium to the stock’s closing price on November 4, 2025. Fairfax has committed up to $1.65 billion in equity to fund the deal, redeem preferred shares, and cover costs. Upon closing — expected in Q2 2026 — Fairfax would hold majority economic interest in the now-private company while McMorrow and key executives continue running operations.

Kennedy-Wilson, a Beverly Hills-based real estate investment manager with roughly $31 billion in assets under management, focuses on multifamily and commercial properties across the United States and Europe.

The lawsuit also accuses McMorrow and other directors of breaching their fiduciary duties by structuring the transaction to evade statutory protections for public shareholders. Taylor is seeking a court declaration that the merger cannot close without the required two-thirds vote, plus an injunction blocking the stockholder vote until the agreement is revised and corrective disclosures are made.

Representatives for Kennedy-Wilson, Fairfax, and the buyer entities did not immediately respond to requests for comment.

This high-stakes Delaware battle could set important precedent for how take-private deals involving existing large shareholders and management are structured going forward, particularly in an environment where activist investors and institutional holders are increasingly scrutinizing insider-led buyouts.

FOLLOW US

Recent Posts

NASA Launches Artemis II Mission, First Crewed Moon Flight Since…

Trump Fires Pam Bondi Amid Epstein Files Controversy

Plane Crashes in Philadelphia Park, Two Injured

Baby Fatally Shot in Brooklyn in Broad Daylight

US Lifts Sanctions on Delcy Rodríguez Amid Venezuela Diplomatic Shift

Cold Case Breakthrough: Ted Bundy Linked to 1974 Utah Murder

Coral Springs Vice Mayor Found Dead, Husband Arrested

Don’t Miss It

Magnitude 4.6 Earthquake Strikes Near Boulder Creek, Shakes Bay Area

By – Rihem AkkoucheChristina Marie Plante Found Alive After 32-Year Mystery

By – Rihem AkkoucheSpaceX, Led by Elon Musk, Prepares for $1 Trillion Public Offering

By – Tyler BrooksDecomposed Body Found in San Jose Vehicle Linked to Missing Man

By – Tyler BrooksU.S. Unleashes Iranian-Inspired Drone in Strike Campaign

By – Tyler BrooksNew York at Risk: 20% of the City Built on Water

By – Tyler BrooksIs X down? Thousands of Users Report Access Problems

By – Tyler BrooksJudge Allows Tiger Woods to Travel Abroad for Medical Treatment

By – Tyler Brooks

Kelly Warner Law Firm Blames USA Herald for Arizona Bar Investigation

In what appears as a desperate attempt to defend multiple allegations of fraud on the courts, the Kelly Warner Law…

By – USA Herald

Aaron Kelly Law Firm Resorts To Attacking Former Client Again On KellyWarnerLaw.com – Pattern Recognized

Attorney Aaron Kelly and his law partner Daniel Warner are currently under investigation by the Arizona Bar for legal misconduct.…

By – Jeff Watterson

Arizona Bar Opens Investigation on Attorney Aaron Kelly

USA Herald recently reported on a developing story involving Attorneys Daniel Warner and Aaron Kelly. Both Warner and Kelly have…

By – Paul O'Neal

Artemis II Crew Begins 10-Day Journey Around Moon After Successful Launch

NASA has launched its Artemis II mission, ushering in the first crewed flight to the vicinity of the moon since…

By – Tyler Brooks

Trump Threatens NATO Exit, Tells Europe to ‘Go Get Your Own Oil’

President Donald Trump intensified his criticism of European allies this week, warning that the United States could abandon long-standing security…

By – Tyler Brooks

Trump Considers Replacing Pam Bondi with Lee Zeldin Amid Epstein Controversy Pressure

President Donald Trump has privately weighed the possibility of removing Attorney General Pam Bondi and installing Environmental Protection Agency Administrator…

By – Tyler Brooks

Trump Defends Iran War in Address but Leaves Key Questions Unanswered

President Donald Trump delivered a nationally televised address Wednesday night seeking to justify the ongoing war with Iran, but his…

By – Tyler Brooks

“NEARING COMPLETION” — But The War Goes On

WHAT MATTERS NOW President Trump delivered his first prime-time address on the Iran war — 33 days after it began.…

By – Samuel Lopez

HUMANITY RETURNS TO THE MOON: NASA’s Artemis II Lifts Off — First Crewed Lunar Mission In 53 Years

WHAT MATTERS NOW Four astronauts are en route to the Moon for the first time since 1972. History is being…

By – Samuel Lopez

HUMANITY RETURNS TO THE MOON: NASA’s Artemis II Lifts Off — First Crewed Lunar Mission In 53 Years

WHAT MATTERS NOW Four astronauts are en route to the Moon for the first time since 1972. History is being…

By – Samuel Lopez

When Allegations Become Weapons How Lawfare Is Being Used In Personal Conflicts

WHAT MATTERS NOW In courtrooms across the country, allegations are not just claims—they are leverage. When the legal system is…

By – Samuel Lopez

Alien Intelligence vs. Artificial Intelligence Who Would Win The Ultimate Unknown Battle

WHAT MATTERS NOW Two of the most powerful unknowns confronting humanity—non-human intelligence and artificial intelligence—are no longer theoretical conversations happening…

By – Samuel Lopez

JD Vance’s Comments That UFOs Might Be Demons Ignites Debate Over Spiritual Threat vs. Extraterrestrial Theory

INSIDE THIS REPORT A sitting Vice President suggests UFOs may not be extraterrestrial—but something far older and more ominous. A…

By – Samuel Lopez

Psychological Warfare At Home – How Alien Narratives Could Be Used To Influence Civilian Populations

INSIDE THIS REPORT Something more sophisticated than rumor may be at play when highly provocative, unverified narratives begin surfacing from…

By – Samuel Lopez

When Speculation Turns Inward – How Alien Narratives Could Reshape Trust In Everyday Life

WHAT MATTERS NOW There is a line between curiosity and destabilization. Recent statements circulating in political and online spaces have…

By – Samuel Lopez

Goliath Ventures Filed for Chapter 11 as Alleged $328M Crypto Scheme Unravels

A Florida crypto firm once promising sky-high returns has collapsed under the weight of federal scrutiny and investor outrage. Goliath…

By – Rihem Akkouche

Ohio State Suspends Fraternity After Student Hospitalization

The case now drawing attention under the headline Ohio State suspends Fraternity has cast a spotlight on campus safety, as…

By – Rachel Moore

Senate Vote on DHS Shutdown Ends Weeks-Long Standoff

The Senate vote on DHS shutdown unfolded in the early hours of Friday, bringing a dramatic pause to a 42-day…

By – Rihem Akkouche

7 Year-Old Girl Dies in Modesto Duplex Fire, Family Devastated

The 7 year-old girl dies in Modesto duplex fire tragedy has left a California community reeling after flames tore through…

By – Rachel Moore

Namibia Blocks Elon Musk’s Starlink in Licensing Setback

In a move that underscores the collision between global ambition and local policy, Namibia blocks Elon Musk’s Starlink, denying the…

By – Rachel Moore

NASA Plan for Moon Base Shifts Course in $20 Billion Lunar Pivot

In a dramatic strategic overhaul, the NASA plan for moon base is taking center stage as the agency abandons its…

By – Rachel Moore

Mike Fincke Space Medical Incident Stuns NASA as Mystery Illness Strikes in Orbit

A routine evening aboard the International Space Station turned into a moment of high-stakes uncertainty when the Mike Fincke space…

By – Rihem Akkouche

Arizona Man Accused of Crucifying Pastor Pushes Judge For A Quick Death Sentence

By Samuel A. Lopez | USA Herald – An Arizona courtroom is now the center of a deeply disturbing case…

By – Samuel Lopez

Trump’s Laser Talk Sparks New Questions About America’s Secret Arsenal

President Donald Trump has once again done what he often does best in moments of war and tension: he dropped…

By – Samuel Lopez

The Northern Lights Return

The Northern Lights have a chance to be visible from several northern U.S. states on Tuesday night, forecasters at the…

By – Jackie Allen

February Unemployment Up as Job Losses Surprise Economists

February Unemployment Up as the latest labor market data revealed weaker-than-expected job growth and a slight increase in the national…

By – Jackie Allen

Late-Night Attack by Venezuelan National at Florida Beach

A Late-night attack by a Venezuelan National has left a Florida community shaken after authorities say a 26-year-old man ambushed…

By – Jackie Allen

When Speculation Turns Inward – How Alien Narratives Could Reshape Trust In Everyday Life

WHAT MATTERS NOW There is a line between curiosity and destabilization. Recent statements circulating in political and online spaces have…

By – Samuel Lopez

Lawmakers Fuel New Disclosure Speculation As Alien Claims Surface In Political Circles

WHAT MATTERS NOW A fresh wave of disclosure speculation is building after explosive remarks attributed to an Australian senator suggested…

By – Samuel Lopez

China Steps Into Iran Conflict as Potential Peacemaker Amid Rising Oil Prices

As the conflict in the Middle East enters its second month, disrupting global energy markets and pushing oil prices higher,…

By – Tyler BrooksINSIDE THIS REPORT A Los Angeles judge has rejected an attempt by Kim Kardashian and Kris Jenner to shield a…

By – Samuel Lopez

Crowds Gather on Florida’s Space Coast as Artemis II Launch Nears

“People going up to the Moon is kind of cool,” eight-year-old Isiah says. He is one of an estimated 400,000…

By – Tyler Brooks

Oracle Announces Major Layoffs Amid Expanding AI Investments

Oracle carried out what employees described as “significant” job cuts on Tuesday, as the technology company continues to ramp up…

By – Tyler Brooks

Health Insurers 19% Claims Refusal Raises Alarm Across ACA Marketplace

A new analysis reveals a striking reality: health insurers 19% claims refusal has become a defining feature of coverage on…

By – Rachel Moore

Hospitals Threatened by Medicaid Cuts Face Growing Crisis Nationwide

A sweeping new analysis warns that hospitals threatened by Medicaid cuts are edging toward a breaking point, with hundreds of…

By – Rachel Moore

Isometric Workouts Gain Attention as Time-Efficient Path to Better Health

For many people, fitness conjures images of long hours spent running on treadmills, powering through burpees or lifting heavy weights.…

By – Tyler Brooks

How Much Screen Time Is Safe for Kids Under Five?

New government guidance recommends that children under five should spend no more than one hour a day on screens, while…

By – Tyler Brooks

New Therapies Offer Hope for Lasting Relief From Hay Fever

A new generation of treatments is renewing hopes that seasonal allergies could one day be controlled at their source, rather…

By – Tyler Brooks

Five Practical Ways Parents Can Curb Kids’ Endless Scrolling

A recent U.S. court decision finding that Meta and Google deliberately engineered addictive social media platforms has resonated with many…

By – Tyler Brooks

Italy Misses Third Consecutive World Cup After Shootout Loss to Bosnia-Herzegovina

Italy, four-time World Cup champions, will not feature at this year’s tournament after a heartbreaking penalty shootout defeat to Bosnia-Herzegovina,…

By – Tyler Brooks

Men’s March Madness Elite 8 Delivers High-Stakes Drama as Title Race Tightens

The madness is reaching its boiling point. The Men’s March Madness Elite 8 has arrived, trimming the 2026 NCAA Tournament…

By – Rihem Akkouche

The World Cup Security Reckoning: Trump Warns Iran Soccer Team About Safety As War Tensions Spill Into Global Sports

By Samuel A. Lopez | USA Herald – A short Truth-Social post from President Donald Trump on Thursday morning is now…

By – Samuel Lopez

Late-Night Attack by Venezuelan National at Florida Beach

A Late-night attack by a Venezuelan National has left a Florida community shaken after authorities say a 26-year-old man ambushed…

By – Jackie Allen

Trump’s War in Iran: Congress Confronts Escalation After U.S. Strikes

Trump’s War in Iran was triggered open conflict, casualties, and renewed constitutional debate in Washington. The crisis intensified following reports…

By – Jackie Allen

Cadillac Names Inaugural Formula 1 Car MAC-26 in Tribute to Mario Andretti Ahead of 2026 Australian Grand Prix Debut

Cadillac has officially revealed the name of its first Formula 1 challenger, confirming that its 2026 car will be called…

By – Ahmed BoughallebNo posts found.

No posts found.

No comments yet. Be the first to comment!

No comments yet. Be the first to comment!